Summary

- Small business tax credits can save you thousands of dollars on your tax bill each year.

- You may be eligible for credits such as the Work Opportunity Tax Credit and Research and Development Tax Credit.

- To claim tax credits, you must file your tax returns accurately and on time.

- A tax professional can help you get the most out of your tax credits.

- If you invest in energy efficiency, you may be eligible for additional tax credits.

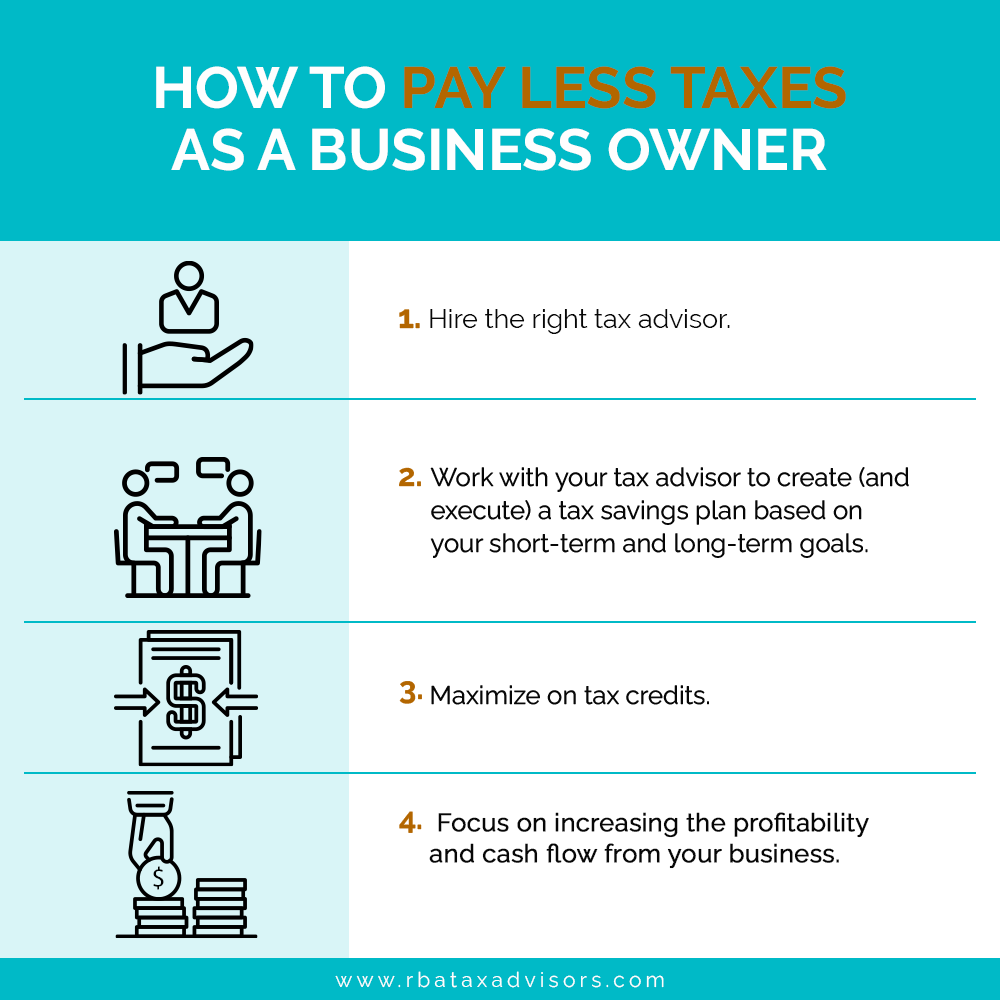

The Importance of Tax Credits for Small Business Owners

Tax credits are more than just a financial perk for small business owners. They’re a strategic tool that can significantly reduce the amount of tax you owe. This makes them a powerful money-saving tool. Unlike deductions, which only reduce your taxable income, tax credits are subtracted from your total tax bill. As a result, understanding and taking advantage of these credits can have a big impact on your business’s bottom line.

First and foremost, tax credits offer immediate financial relief. When you claim a credit, it lowers your tax liability on a dollar-for-dollar basis. This means more money remains in your business, which you can use to reinvest, pay down debt, or grow operations. For many small businesses, this can be the difference between survival and failure.

“Small business owners who take advantage of tax credits can save thousands of dollars on their taxes each year, which can then be used to help grow their business.” — IRS Tax Credit Guide

Instant Cash Flow

For small businesses operating on a tight budget, instant cash flow is essential. Tax credits can provide this by directly reducing your tax bill. If you owe $5,000 in taxes but have a $2,000 tax credit, you only need to pay $3,000. This can help you manage your cash flow more effectively.

Boosting Business Expansion Possibilities

In addition to providing financial assistance, tax credits boost expansion possibilities. When you save on taxes, you can reinvest the resources back into your business. This could involve hiring more employees, buying new machinery, or extending your product range. The trick is to figure out which credits are applicable to your business and fully utilize them.

Take for instance, the Research and Development Tax Credit. This is designed to stimulate innovation by letting businesses claim a credit for research costs. So, if you’re working on creating new products or enhancing current ones, you could get a tax cut for your hard work.

Promoting Eco-Friendly Business Operations

Another advantage of tax credits is that they promote eco-friendly business operations. Take the Energy Efficiency Tax Credit, for example. This credit gives businesses a tax break for investing in renewable energy or energy-saving equipment. This benefits you in two ways. First, it lowers your tax bill. Second, it reduces your energy costs in the long run. Plus, you’ll be doing your part for the environment and boosting your brand’s image at the same time.

Nowadays, many customers prefer to patronize businesses that are mindful of their environmental impact. As a result, taking advantage of green tax credits can also serve as a marketing strategy, drawing more customers to your business.

Common Tax Credits for Small Business Owners

Small business owners have access to a variety of tax credits. The first step to saving the most on your taxes is to understand which credits you are eligible for. Let’s look at some of the most common credits.

General Business Credit

The General Business Credit is a bucket of credits that you can claim on your tax return. This includes credits for things like investing in renewable energy, offering childcare for your employees, and hiring folks from certain target groups. Each credit has specific requirements, so it’s important to do your homework to see which ones apply to your business. For example, there are tax benefits for minority-owned and women-owned businesses that could be relevant.

Exploring the R&D Tax Credit

Designed to incentivize businesses to invest in innovation, the Research and Development (R&D) Tax Credit could be a big help to your small business. If you’re spending money on creating new products or improving existing ones, you could qualify for this credit. It’s an excellent way to recoup some of the costs associated with your research activities.

Work Opportunity Tax Credit (WOTC)

Small business owners can avail of the Work Opportunity Tax Credit (WOTC) when they hire individuals from certain groups who have had significant barriers to employment. This includes veterans and the long-term unemployed. The WOTC not only reduces your tax bill but also supports social responsibility by helping those in need find work.

Energy Efficiency Tax Credit

With the Energy Efficiency Tax Credit, businesses that invest in energy-efficient upgrades are rewarded. This could include installing solar panels, upgrading HVAC systems, or purchasing energy-efficient appliances. This credit not only reduces your tax liability, but it also decreases your energy bills in the long run. For more insights on optimizing your business finances, explore these small business tax planning tips.

Wrapping up, tax credits are essential for small business owners. By knowing and using these credits, you can decrease your tax liability, put money into your business’s growth, and use sustainable practices. In the next part, we’ll look at strategies to get the most out of your tax credit benefits.

Using Tax Software and Tools

For small business owners, taking advantage of tax software and tools is a smart move in the digital age. These tools can uncomplicate the intricate process of tax filing, ensuring you don’t overlook any credits you’re eligible for. Most importantly, tax software can help you maintain your financial records, making it easier to claim credits accurately.

Several tax software solutions offer automatic updates on changes in tax laws, which are vital for maintaining compliance. They usually provide step-by-step instructions throughout the filing process to make sure you claim all the credits you’re entitled to. Check out TurboTax, QuickBooks, or H&R Block, which have features specifically for businesses.

Seeking Advice from a Tax Expert

Although software tools are useful, seeking advice from a tax expert can enhance your tax planning. Tax experts offer knowledge and experience that software cannot compete with. They can offer tailored advice based on your particular business circumstances and assist you in understanding complicated tax regulations.

When collaborating with a tax professional, make sure they have a background in small business. They can help you find more obscure credits you might be eligible for, ensuring you get the most savings possible. In addition, they can help you with strategic planning for future tax years, allowing you to make smart decisions that are in line with your business objectives.

Plan Your Finances and Time Your Claims

Claiming your tax credits at the right time can make a big difference in how much you benefit from them. By carefully managing your finances and strategically planning when to claim your credits, you can get the most out of your tax credits. This will involve keeping a close eye on your business finances all year round.

A good approach is to make sure your business expenses match up with any available credits. So, if you’re going to buy energy-efficient equipment, try to time your purchase with when tax credits are available. This will boost your savings. Regular financial reviews can help you spot these opportunities and take advantage of them quickly.

Year-End Financial Checkup

A year-end financial checkup is an important part of strategic tax planning. This checkup gives you a chance to evaluate your financial health, see where you can improve, and plan for the next tax season. During this checkup, concentrate on figuring out what credits you can still get before the year is over.

Think about collaborating with your accountant or tax expert to guarantee you take full advantage of all qualifying credits. They can assist you in examining your financial records, pinpointing potential tax-saving possibilities, and making any necessary modifications to improve your tax situation.

Putting Off Expenses and Speeding Up Income

Putting off expenses and speeding up income are strategies that can help you manage your tax liability more effectively. By putting off expenses to the next tax year, you can increase your taxable income for the current year, potentially qualifying for additional credits. Conversely, speeding up income can help you take advantage of credits that are based on your revenue.

For example, if you think you’ll be in a lower tax bracket next year, putting off expenses could lower your tax bill this year. Conversely, if you think you’ll make more money next year, bringing in income sooner could let you get the most out of credits based on your current finances.

Prepare for Future Tax Seasons

It’s important to prepare for future tax seasons to ensure your business’s long-term success. By predicting your financial performance and potential tax liability, you can make decisions that are in line with your business’s goals. This includes saving money for future tax payments and identifying credits you might be eligible for in the future.

Think about making a tax calendar that highlights crucial due dates and filing times. This will assist you in staying organized and ensuring that you do not overlook any chances to claim credits. Furthermore, frequently discuss your tax strategy with your accountant or tax expert to adjust to any changes in tax laws or your company’s situation.

Assessing Your Business Structure and Tax Approach

The structure of your business can have a big effect on your ability to claim tax credits. Different business structures, like sole proprietorships, partnerships, or corporations, can have different tax consequences. It’s important to understand these differences in order to make the most of your tax approach and get the most credits possible.

How Business Structure Affects Tax Credits

Depending on the structure of your business, you may file taxes differently and be eligible for different credits. Sole proprietorships and partnerships, for example, often qualify for pass-through deductions that can lower your taxable income. However, corporations may qualify for other credits that aren’t available to other business structures.

It’s a good idea to review your current business structure with a tax expert. They can explain the advantages and disadvantages of each structure and help you decide if a change would be beneficial for your tax situation. This review could result in considerable tax savings and improve your overall financial situation. For more insights, consider exploring small business tax planning tips.

Grasping the Limitations of Pass-Through Entities

Income is passed directly to the owners in pass-through entities, such as sole proprietorships and partnerships. They then pay taxes on this income. While this structure has its benefits, it also has its drawbacks. Knowing these drawbacks can help you manage your tax liability more effectively.

For instance, the Qualified Business Income Deduction permits suitable pass-through businesses to subtract up to 20% of their qualified business income. Nevertheless, income thresholds and other restrictions might hinder your capacity to claim this deduction. Knowing these restrictions can aid you in planning your finances properly.

Think About Retirement Plan Contributions

Not only is contributing to a retirement plan a wise financial decision, but it can also be a tax-saving strategy. Retirement plan contributions can lower your taxable income, making you eligible for certain credits. For small business owners, establishing a retirement plan can provide both personal and business tax benefits.

You can reduce your tax liability and save for retirement by setting up a Simplified Employee Pension (SEP) IRA or a Solo 401(k) for your small business. These plans also provide tax advantages for your employees. Speak with a financial advisor to figure out which plan is the best fit for your business.

Eco-friendly Tax Credits and Sustainability

Eco-friendly tax credits are intended to motivate businesses to adopt sustainable practices. These credits incentivize investments in renewable energy, energy-efficient equipment, and green initiatives. By utilizing these credits, you can lower your tax liability while also contributing to a greener future.

If you put money into things like solar panels or wind turbines, you could get a lot of tax credits. You’ll pay less in taxes and spend less on energy in the long run. Plus, people will think better of your brand because you’re showing that you care about the environment.

- Renewable Energy Investment Credit: This credit is available to businesses that invest in renewable energy sources like solar or wind.

- Energy-Efficient Commercial Buildings Deduction: This deduction is for businesses that make energy-efficient improvements to their buildings and allows them to claim a tax break.

- Clean Vehicle Tax Credit: This credit is for businesses that purchase electric or hybrid vehicles and is intended to encourage the use of environmentally friendly transportation.

By incorporating green practices into your business strategy, you can benefit the environment and also receive financial incentives. Understanding and taking advantage of these credits can improve your bottom line and support a sustainable future.

Why You Should Invest in Renewable Energy

Putting your money in renewable energy isn’t just about being environmentally friendly; it’s also a great way to save money for your business. Renewable energy investments can drastically cut your operating costs by reducing your utility bills. And on top of that, they can qualify you for a variety of tax credits and incentives, which can effectively reduce your tax bill.

These investments can also boost your business’s image. More and more customers are choosing to support businesses that are environmentally aware. By showing your dedication to sustainability, you can draw in a wider customer base and potentially increase your sales.

Eligibility for Clean Vehicle Tax Credits

Businesses that buy electric or hybrid vehicles can take advantage of Clean Vehicle Tax Credits. To be eligible, the vehicles must satisfy certain requirements set by the IRS. These requirements include being used mainly for business and meeting specific environmental standards.

These credits can significantly lower the cost of purchasing new vehicles, making it more manageable for businesses to switch to a more sustainable fleet. Additionally, they assist in reducing your overall carbon footprint, aligning your business practices with environmental objectives.

Benefits of Energy Efficiency Upgrades

- Switch to energy-efficient lighting and HVAC systems.

- Use programmable thermostats to better manage energy use.

- Upgrade to appliances rated by Energy Star.

There are many benefits to making energy efficiency upgrades. Not only can you qualify for deductions and credits that lower your tax bill when you upgrade your equipment and facilities, but you also reduce your energy consumption, saving you money on utility bills in the long run.

On top of that, these improvements often meet the criteria for local and state incentives, which offer more financial advantages. Before making any modifications, consult with your local government or utility provider to find out what programs are offered.

Wrapping Up: Using Tax Credits to Boost Your Business

To sum up, tax credits are a potent weapon for boosting small business owners. They offer financial help, spur expansion, and promote sustainable practices. By knowing and utilizing available tax credits, you can significantly cut your tax bill and reinvest in your business’s growth. For more insights, explore our small business tax planning tips.

Get the most out of these benefits by teaming up with a tax expert who can walk you through the process and help you claim every credit you qualify for. With a little foresight and some smart investments, tax credits can become a key part of your business plan, fueling growth and long-term stability.

Common Questions

Tax credits can be confusing, and many business owners have questions about how they work. Here are some common questions and their answers to help you understand this important aspect of your business finances.

What are the typical tax credits for small businesses?

The typical tax credits for small businesses are the General Business Credit, Research and Development Tax Credit, Work Opportunity Tax Credit, and Energy Efficiency Tax Credit. Each of these credits has its own eligibility requirements, so it’s crucial to figure out which ones are applicable to your business.

What is the difference between a tax credit and a tax deduction?

A tax credit directly decreases the amount of tax you have to pay, while a tax deduction reduces your taxable income. Tax credits are usually more beneficial because they reduce your tax bill on a dollar-for-dollar basis. Deductions, however, only reduce your income by a percentage of your marginal tax rate. For more information, visit the IRS website on credits and deductions.

Is it possible to retroactively claim tax credits?

Yes, in certain situations, you can retroactively claim tax credits. This typically requires filing an amended tax return for the year you were eligible for the credit. Keep in mind, there are time restrictions on how far back you can amend a return, so it’s crucial to take action as soon as possible.

Speak to a tax expert to check if you qualify for any retroactive credits and to make sure you’re amending your return properly.

What if I mess up my tax credit claim?

If you mess up your tax credit claim, you might have to file an amended return to fix the mistake. The IRS might also contact you about the mistake and ask for more documentation or payment. It’s important to fix any mistakes quickly to avoid fines or interest.

Collaborating with a tax expert can help you avoid errors and ensure the accuracy of your tax credit claims. They can also help you deal with any problems that may come up with the IRS.

Are tax credits different in each state?

Absolutely, tax credits can differ from state to state. Besides the federal tax credits, numerous states provide their own credits and incentives for businesses. These may encompass credits for creating jobs, investing in renewable energy, among other programs.

Make sure you look into both federal and state tax credits to make sure you’re not missing out on any opportunities. You can get more information on state-specific credits from your state’s Department of Revenue or a local tax professional. For additional guidance, you might also consider exploring new business tax considerations to ensure you are fully informed.

Should I invest in green energy for tax credits?

Yes, investing in green energy is a great idea. Not only will you save money in the long run, but you could also qualify for significant federal and state tax credits, lowering your initial investment.

Small business owners often overlook the various tax credits available to them, which can significantly reduce their tax liability. Understanding and utilizing these credits can provide substantial savings. For detailed information on available credits and deductions, visit the IRS website to explore options that might benefit your business.

Not only can these investments boost your business’s reputation, but they can also attract customers who care about the environment. By going green, you can make your business stand out as an environmentally responsible leader.

Small business owners often struggle with understanding the various tax credits available to them. By staying informed and utilizing these credits, they can significantly reduce their tax burden. It’s crucial to keep up with current regulations and consult with a tax professional to maximize these benefits. For more detailed information, you can visit the IRS website which provides comprehensive guidance on business tax credits and deductions.