In a Nutshell

- Reducing taxes is important for business growth as it provides more funds for reinvestment.

- Maximizing deductions and tax credits are essential strategies to lower your tax bill effectively.

- Proper end-of-year tax planning can help you defer income and speed up expenses for better tax results.

- Selecting the right retirement plan can offer significant tax advantages and future savings.

- Working with a tax expert ensures compliance and optimizes your tax-saving strategies.

Quick Guide to Smart Tax Savings for Your Business

Running a business is not just about making a profit; it’s also about keeping as much of it as you can. That’s why reducing taxes is a crucial part of ensuring your business flourishes. When you save on taxes, you can put that money back into your business, helping it grow and prosper.

The Importance of Minimizing Taxes for Business Expansion

Minimizing taxes isn’t just about pocketing more money right now. It’s a calculated decision that can greatly affect the long-term expansion and viability of your business. When you pay fewer taxes, you have more capital to put back into your business. This could be in the form of hiring additional staff, broadening your range of products, or breaking into new markets.

First and foremost, handling your tax liability in an efficient manner keeps your business financially robust and competitive. As such, it’s important to put smart tax-saving strategies into action that are in line with your business objectives.

Top Tactics to Decrease Your Tax Expenses

There are a number of tactics you can use to decrease your company’s tax expenses. These tactics are not just about reducing costs; they’re about being financially savvy and understanding how the tax system benefits you. Here are some top tactics to think about:

- Take Full Advantage of Deductions: Use all the deductions you can to lower your taxable income.

- Make Use of Tax Credits: Know and apply for tax credits that can directly lower your tax liability.

- Plan Your Finances at Year-End: Use strategies like accelerating expenses or deferring income to optimize your tax situation.

- Choose the Right Retirement Plans: Choose retirement plans that offer tax benefits and are in line with your financial goals.

- Hire a Tax Professional: Work with experts to make sure you’re compliant and maximizing tax savings.

Maximizing Deductions

Deductions are a great way to lower your taxable income. They let you subtract certain expenses from your total income, which can greatly lower the amount of tax you owe. But to maximize deductions, you need to know what deductions you’re eligible for and how to properly claim them.

Business Deductions You Should Take Advantage Of

There are a number of standard business deductions that many businesses are able to utilize. These include costs like office supplies, travel, and utilities. To get the most out of these deductions, make sure to keep a detailed record of all your business expenses throughout the year. This will ensure you don’t miss out on any chances to lower your tax bill.

Lesser-known Deductions You May Not Be Aware Of

While there are common deductions that most businesses are aware of, there are also some deductions that are frequently overlooked. For example, if you work from home, you may be able to deduct a portion of your rent or mortgage, utilities, and maintenance costs as a home office deduction.

One often forgotten deduction is the expense of ongoing education or training for you and your team. Enhancing skills and knowledge is not only advantageous for your business but can also lower your taxable income.

Properly Recording Your Deductions

It is important to properly record your deductions to ensure you can claim them during tax season. Utilize accounting software to log all your expenses and keep your receipts and invoices in order. This will simplify the process of filing your taxes and make sure you claim every deduction you are eligible for.

Furthermore, you should think about hiring a tax expert to go over your financial records and discover any deductions you may have overlooked. They can provide useful advice and make your tax filing process more efficient.

How Tax Credits Can Benefit You

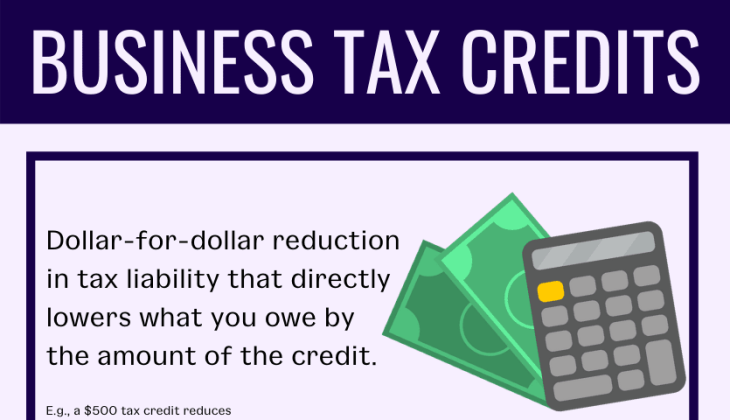

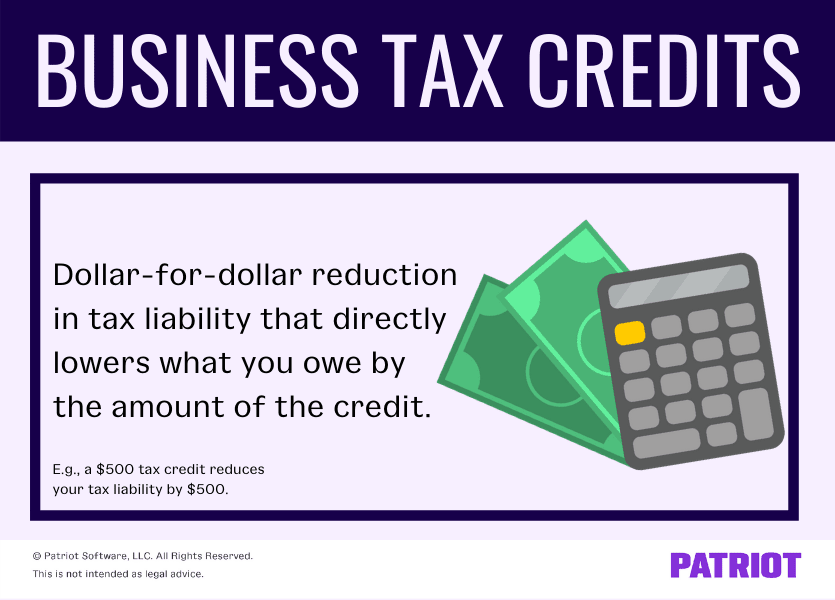

Another way to decrease your tax bill is by using tax credits. Unlike deductions, which decrease your taxable income, tax credits decrease your tax bill directly. This means they can greatly impact your overall tax liability.

How Tax Credits and Deductions Differ

Knowing how tax credits and deductions differ is important for successful tax planning. Deductions reduce your taxable income, while credits offer a dollar-for-dollar reduction in the amount of tax you owe. This makes credits especially useful because they can result in significant tax savings.

For instance, if you’re eligible for a $1,000 tax credit, your tax bill decreases by $1,000. On the other hand, a $1,000 deduction could only lower your tax bill by $250, based on your tax rate.

Common Business Tax Credits

Businesses have a variety of tax credits at their disposal that can greatly lower their tax burden. Two well-known credits are the Research and Development (R&D) tax credit, which motivates businesses to invest in new ideas, and the Work Opportunity Tax Credit, which encourages the hiring of individuals from specific targeted groups.

In order to be eligible for these credits, there are certain conditions that you must meet and proof that you must provide. It’s essential that you look into and comprehend the conditions for each credit to make sure you qualify.

How to Qualify for Tax Credits

Getting tax credits usually involves some strategic planning and paperwork. Here’s what you need to do to qualify:

- Find out what tax credits are available and see if your business is eligible for any of them.

- Keep thorough records and paperwork to back up your claims.

- Check with a tax expert to make sure you’re meeting all the criteria.

- Submit the required forms and applications along with your tax return.

By doing these things, you can get the most out of your tax credits and lower your overall tax bill in a big way.

Strategies for End-of-Year Tax Planning

As the year comes to an end, it’s important to take steps to ensure your tax situation is as good as it can be. Planning your taxes at the end of the year can help you control your taxable income and make the most of your deductions and credits. By strategically planning when you receive income and pay expenses, you can greatly lower the amount of tax you owe. For more detailed guidance, consider exploring tax planning strategies and tips for small businesses.

Speed Up Business Expenses Before the Year is Over

An effective method is to speed up business expenses before the year is over. This involves making purchases or payments that you would otherwise put off until the next year. By doing this, you can increase your deductions for the current tax year. For more strategies, check out these top year-end tax strategies to boost your business bottom line.

Let’s say you’re planning to buy new office equipment. Why not buy it before December 31st? This will allow you to deduct the cost in the current tax year, reducing your taxable income.

In addition, consider prepaying expenses like rent, insurance, or utilities. You can deduct these payments in the year you make them, which gives you immediate tax benefits.

Postponing Income for Future Benefits

A different approach is to postpone income until the next year. This strategy is especially beneficial if you anticipate being in a lower tax bracket the following year. By postponing income, you can decrease your taxable income for the current year and possibly pay less in taxes in total.

Consider postponing the completion of projects or delaying sending invoices until January to defer income. However, make sure this strategy aligns with your cash flow needs and business goals.

As businesses strive to maximize their profits, understanding tax credits can be a crucial factor in reducing expenses. Many companies are unaware of the various credits available to them, such as the Employee Retention Tax Credit (ERTC). For businesses that experienced shutdowns or significant revenue declines, exploring ERTC tax relief options can provide substantial financial benefits. Taking advantage of these opportunities not only aids in compliance but also enhances overall financial health.

Keep in mind, balancing deferred income with maintaining enough cash flow to meet your business’s immediate needs is crucial.

Intelligent Timing of Acquisitions and Payments

- Plan large purchases strategically to take full advantage of deductions.

- Prepay expenses where possible to maximize current-year deductions.

- Review unpaid invoices and consider delaying invoicing if it is beneficial.

By strategically timing your acquisitions and payments, you can maximize your tax position and take full advantage of available deductions. This strategy requires careful planning and consideration of your company’s financial needs.

First and foremost, make sure that any choices you make are in line with your long-term business plan and won’t jeopardize your financial security.

Engaging a tax expert to assess your alternatives and execute the most effective strategies for your business is a wise move.

The Tax Advantages of Retirement Plans

Not only do retirement plans allow you to prepare for your future, but they also come with substantial tax benefits. By contributing to a retirement plan, you can lower your taxable income and potentially decrease your tax bill. This is a win-win scenario that benefits both your current financial well-being and your future security.

It’s essential to choose the best retirement plan for your business. Different plans have different benefits, so you need to know your choices and choose one that matches your financial goals.

Selecting the Best Retirement Plan

When it comes to picking a retirement plan, you need to take into account elements like the size of your business, the needs of your employees, and the limits of your contributions. The most popular choices are SEP IRAs, SIMPLE IRAs, and 401(k) plans. Each of these plans has its own set of characteristics and advantages, so it’s crucial to take the time to assess them thoroughly.

For example, a SEP IRA is a great option for small businesses because it’s easy to set up and flexible. You can make large contributions that you can deduct from your taxable income.

How Retirement Contributions Can Help You Save on Taxes

When you contribute to a retirement plan, you reduce your taxable income and can save a lot on taxes. For instance, if you contribute $10,000 to a SEP IRA, you can reduce your taxable income by that amount, which will lower your tax bill.

Not only do retirement contributions offer instant tax benefits, they also grow tax-free. This means you won’t pay taxes on the earnings until you retire and start making withdrawals. This allows your investments to build up over time, which can significantly boost your retirement savings.

Work with a Tax Expert

One of the most effective ways to guarantee that your business gets the most out of tax savings is to collaborate with a tax expert. These professionals have the expertise and experience to navigate complicated tax laws and pinpoint areas for savings. They can offer useful advice and direction that is customized to the specific needs of your business.

Not only can a tax professional help you maximize your tax savings, but they can also help you stay compliant with tax laws and regulations. This is crucial for avoiding expensive penalties and keeping your business financially healthy.

How to Choose a Trustworthy Tax Advisor

If you’re in the market for a tax advisor, make sure to find one who has a solid background in your field and a history of successful cases. Get recommendations from other business owners and check out reviews to make sure you’re picking a trustworthy expert.

In your first meeting, talk about your company’s financial objectives and ways to save on taxes. A competent consultant will pay attention to your requirements and suggest tailored strategies to assist you in reaching your goals.

Collaborating with Professionals to Optimize Tax Savings

Working with a tax expert can optimize your tax savings and provide reassurance. They can manage complex computations, guarantee precise filing, and keep you updated on any changes in tax regulations that could impact your company.

Furthermore, a tax advisor can assist you in creating a long-term tax strategy that fits with your business’s expansion and financial objectives. This proactive strategy can result in substantial savings and contribute to your business’s success.

Keeping Up with Tax Regulations

It is crucial to stay on top of tax regulations to avoid fines and keep your business’s image intact. A tax specialist can help you understand and fulfill your tax duties, guaranteeing you stay within all relevant rules.

They can also guide you on how to keep records, report requirements, and other matters related to compliance, helping you avoid common traps and expensive errors.

You can concentrate on expanding your business and reaching your financial objectives without the fear of possible legal problems by remaining compliant.

Preparing Your Business Tax Strategy for the Future

Keeping up with the fast-paced business world doesn’t just require innovation and growth, but also strategic tax planning. Preparing your tax strategy for the future means regularly reviewing and updating your approach to make sure it aligns with your ever-changing business goals and the constantly shifting tax landscape. For small businesses, exploring tax planning strategies and tips can be crucial in navigating these changes effectively.

Consistently Assess and Revise Tax Plans

Changes in tax laws and regulations can occur often and may affect your business’s tax liabilities and potential savings. As such, it’s important to consistently assess and revise your tax plans to ensure compliance and optimize savings. Make sure to allocate time each year to assess your existing tax strategy and make any needed changes based on modifications in your business activities or the tax code.

Working with a tax professional during this process can give you valuable insights and make sure your strategies stay effective and in line with your financial goals.

Staying Current with Tax Law Changes

It is crucial to stay updated on changes in tax laws to ensure your tax strategy is compliant and effective. New laws can introduce new deductions, credits, or compliance requirements that may impact your business. Keep yourself informed by subscribing to updates on tax news, attending workshops, or seeking advice from a tax advisor who can offer up-to-date information and guidance.

By getting a handle on these changes, you can adjust your tax strategy in a proactive manner to seize new opportunities or lessen potential challenges.

- Make sure to go over your tax strategies every year to ensure they’re in line with the current laws.

- Keep yourself updated about changes in tax laws through reliable sources.

- Seek advice from a tax professional to understand how new laws will affect you.

- Change your tax strategy if needed to stay legal and maximize savings.

Commonly Asked Questions

Answering the most common questions about business tax strategies can help make the process clearer and enable you to make educated decisions. For example, understanding whether education expenses are deductible can be crucial for business owners. Here are some commonly asked questions and their answers.

What are some typical tax write-offs for small businesses?

Typical tax write-offs for small businesses include costs such as office supplies, travel, and utilities. You can also write off expenses related to advertising, employee benefits, and professional services. It’s crucial to maintain detailed records of these costs to ensure you can accurately claim them on your tax return.

Also, don’t forget about deductions for home office costs, vehicle usage, and ongoing education, which can also result in substantial tax savings.

What are the advantages of tax credits for my business?

Tax credits give a dollar-for-dollar reduction in your tax liability, which makes them a very attractive proposition for businesses. They can dramatically reduce the amount of tax you have to pay, freeing up money for reinvestment into your business. The Research and Development (R&D) tax credit and the Work Opportunity Tax Credit are some of the most popular credits.

When is it a good idea to defer income?

If you expect to be in a lower tax bracket next year, you might want to think about deferring income. This could decrease your taxable income this year and possibly reduce your total tax bill. But remember, you need to weigh the benefits of deferring income against the need to keep enough cash flow for your business. For more insights, you can explore strategies like the ERTC tax credit to manage your finances effectively.

How can retirement plans aid in lowering taxes?

Retirement plans aid in lowering taxes by enabling you to contribute dollars before they are taxed, which decreases your income that is taxable. Contributions grow with tax deferred, meaning you will not pay taxes on the earnings until you take them out in retirement. This can result in significant tax savings and aid your financial goals in the long-term.

Picking the best retirement plan, like a SEP IRA or 401(k), can offer more tax advantages and fit with your company’s financial goals.

- Putting money into retirement plans can lower your taxable income because those contributions are tax-deductible.

- Your retirement savings can grow over time because your earnings are tax-deferred.

- Pick a plan that best suits the size of your business and the needs of your employees to get the most out of it.

What are the benefits of hiring a tax professional?

Getting a tax professional on your team can help you save money on your taxes and keep you in line with complex tax laws. They have the know-how and experience to navigate the world of taxes, find ways for you to save money, and give you advice that’s specific to your business.

How frequently should I reassess my tax plan?

You should reassess your tax plan at least once a year, or whenever there are substantial changes in your business or in tax laws. Regular reassessments ensure that your plan is still effective and in line with your financial objectives. Getting advice from a tax professional during these reassessments can be very helpful.

What should I do if a tax law changes?

If a tax law changes, it’s crucial to grasp how it affects your business and to modify your strategy as needed. Stay up to date through reliable sources like tax news updates or your tax advisor. Make the necessary changes to your tax plan to stay in compliance and maximize savings under the new law.

Adapting to changes in advance will help your business to continue to thrive and take advantage of new opportunities to save on taxes.

So, in a nutshell, reducing your business taxes is a strategic decision that promotes growth and financial stability. With the use of efficient strategies to save on taxes, staying updated on tax laws, and working alongside professionals, you can improve your tax situation and enable your business to flourish.